Copper Price Hits New Highs in 2026

Copper Price Hits New Highs in 2026 – What’s Driving the Rally?

At the start of 2026, copper prices have once again broken historical records. What’s behind this surge?

On January 5, LME copper prices touched $13,000 per ton for the first time, briefly approaching $13,020 intraday. This breakthrough follows an impressive year: in 2025, copper gained over 43%, marking its strongest annual performance since 2009.

Among the six major industrial metals traded on the LME, copper was the top performer in 2025 — and this was no coincidence.

1. A Historical Perspective from the Charts

2025 was a breakout year not seen in over a decade. Looking at annual copper price changes on the LME:

· 2009: a post-financial crisis rebound (+100%+)

· The following decade saw cyclical swings, but nothing comparable

· 2025: gains of around 42%–43%

The difference?

· 2009 was a crisis recovery.

· 2025’s rally happened under normal economic conditions.

This suggests copper is being repriced.

---

2. Persistent Supply-Side “Bleeding”

In 2025, multiple key copper mines faced significant output disruptions, including:

· Grasberg in Indonesia

· Kamoa-Kakula in the DRC

Tensions have continued into 2026. Recent strikes at Chile’s Mantoverde copper mine have reignited market concerns.

Al Munro, Senior Base Metals Strategist at Marex, noted: “This is a spec-driven rally. The market still sees upside, especially in Q1 2026, with many waiting for a pullback now forced to enter.”

ING’s view is even clearer: “Years of underinvestment + ongoing mine disruptions leave the market with almost no buffer.”

3. What’s Amplifying the Move: “Tariffs + Stockpile Mismatch”

Recent expectations that the U.S. may reimpose copper tariffs have redirected global copper flows. The result?

· Traders accelerating shipments to the U.S.

· Rising U.S. inventories

· Tighter physical supply elsewhere

UBS highlights a key imbalance:

· The U.S. holds about 50% of global copper stocks

· But accounts for less than 10% of global demand

👉 Stockpiles are concentrated where they aren’t being consumed.

👉 The rest of the world is effectively left short of copper.

---

4. The Physical Market Is Already Telling the Story

A key signal from the LME right now:

· Persistent backwardation in the cash-to-3-month spread

This usually happens for one reason: genuine near-term tightness.

From mine disruptions and tariff distortions to structural inventory imbalances, this copper rally isn’t just sentiment-driven. It reflects:

· The culmination of long-term supply underinvestment

· Policy-driven market distortions

· Money following the narrative

$13,000/ton looks more like a milestone than the final chapter.

Remarks: This analysis is by Yuner, Canada

-

The Rainy Season is Coming – Is Your Drainage Pump Ready?

– Is Your Drainage Pump Ready?

넶4 2026-05-27 -

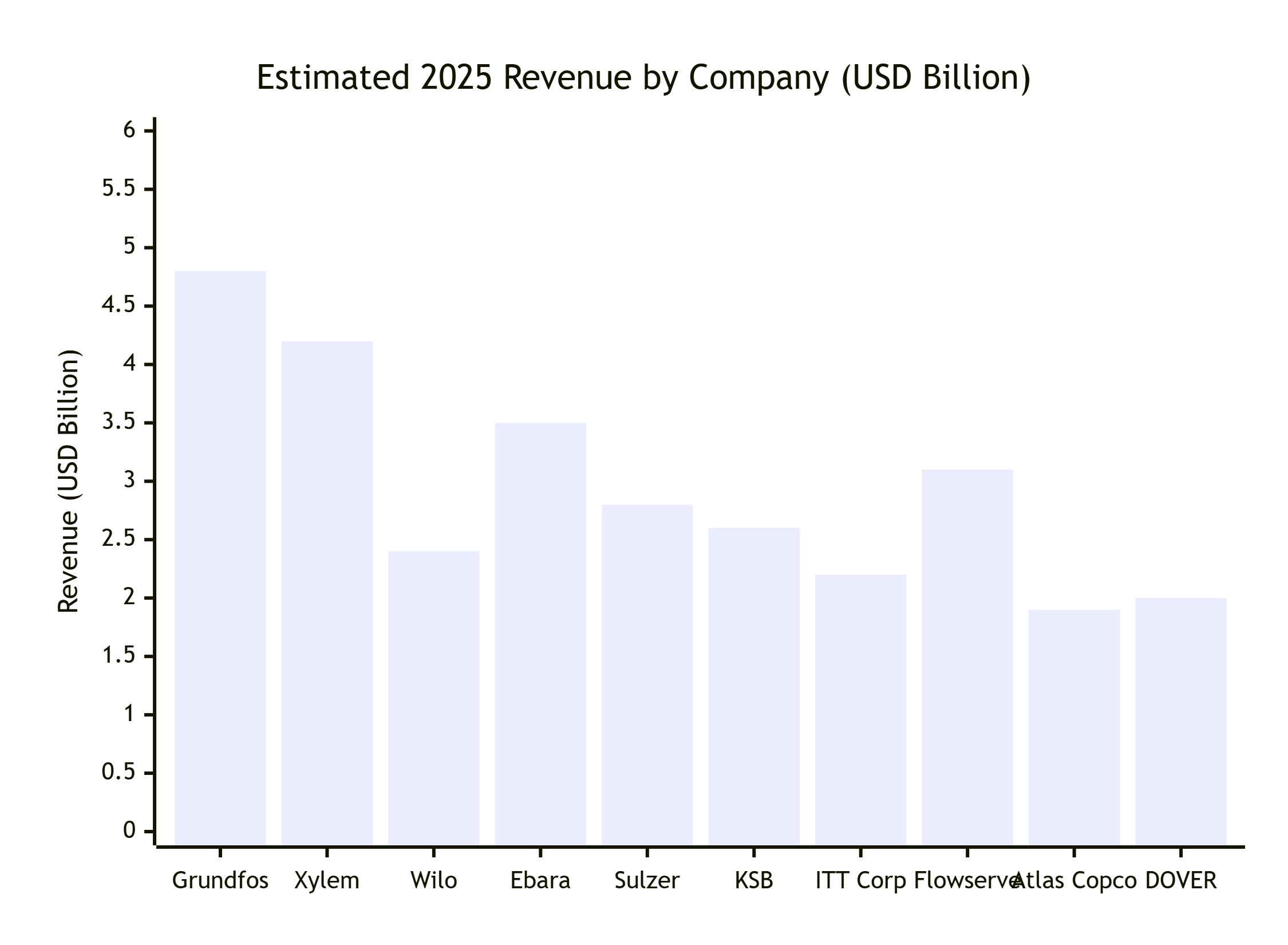

2025 Global Pump Industry Sales Ranking: Key Players & Market Trends

Key Players & Market Trends

넶11 2026-05-12 -

Celebrating Labour Day: The Fluid That Moves the World

The Fluid That Moves the World

넶18 2026-04-30 -

New Opportunities for the Pump Industry in the AI Era

The Liquid Cooling Pump & Valve Market Takes Off

넶22 2026-04-24